The financial space is rife with confusing acronyms, but FICO is one that almost everyone should know. That’s because when discussing FICO, it’s usually your credit score that’s at the center of the conversation. And your credit score is one of the most important and critical pieces of your personal financial mosaic.

But what is FICO? How does it work? Why do you need to know all of this? We’ll get into it below.

What FICO means

Your FICO score is a credit score — not necessarily THE credit score. FICO actually stands for “Fair Isaac Corporation,” which is a private company that creates credit scores for creditors and lenders. As you likely know, your credit score (or FICO score, in this case) serves as your financial reputation, and it gives lenders an idea of how likely you are to pay them back if you borrow from them.

From the Consumer Financial Protection Bureau:

“FICO stands for the Fair Isaac Corporation. FICO was a pioneer in developing a method for calculating credit scores based on information collected by credit reporting agencies. Today, other companies also have credit scoring formulas (“models”), but most lenders still use FICO scores when deciding whether to offer you a loan or credit card, and in setting the rate and terms. Banks may also use FICO scores when approving checking and savings account applications and setting the terms of those accounts.”

What’s a FICO score?

Your FICO score is the credit score that the company, FICO, calculates based on your credit report. It’s a three-digit number, usually between 300 and 850. The closer your FICO score is to 850, the more likely you are to be approved for a loan — and to get a better interest rate.

Again, there are other companies that calculate credit scores, but FICO is the most widely used, which is why you’re most likely to hear about it. As for how the numbers break down? Here’s a chart from FICO’s website to show what a potential score means:

How your FICO score is calculated

So, just how is your FICO score calculated? How can you try and get an “exceptional” score of more than 800?

There are several things that go into the calculation. Again, we’ll go straight to the source — here’s what FICO says determines a score:

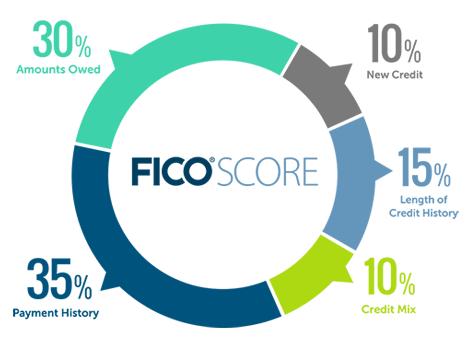

“FICO Scores are calculated using many different pieces of credit data in your credit report. This data is grouped into five categories: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%) and credit mix (10%).”

Here’s a visual:

In all, FICO attempts to take a wide look at your financial history — including your payment history, current debt levels, etc. — in order to calculate your score. And remember, this is meant to be something of a truncated version of your credit score; sort of a quick-and-easy way to gauge your creditworthiness without digging too far into the details.

Also keep in mind that your score can and will change, and that if you check your credit score using any number of websites out there, it may vary a bit.

Like what you see? Get more content sent directly to your inbox! Sign up for the Money Vehicle Movement Newsletter!

More from Money Vehicle: